Precision Machine Tools as a Potential Bottleneck for Humanoid Robotics

The only pure-play publicly traded precision machine tool manufacturer that could potentially be part of this bottleneck.

In April 2025, Bank of America Global Research published a report on humanoid robotics that put a frequently overlooked bottleneck in the spotlight. The core idea: for the expected ramp-up from today’s few thousand units to eventually millions of robots per year to succeed, you need high-precision machine tools on which the precision parts of robot gearboxes are ground. Globally, these come from a handful of European and Japanese companies whose output cannot be expanded at will. With that, the bottleneck thesis moves from a niche argument among specialist robotics investors into a mainstream sell-side view: externally validated, but no longer undiscovered.

Anyone wanting to play this bottleneck through the public markets ends up, in the West, at exactly one listed name: a Swiss family business founded in 1863 that has defended a de facto duopoly in a single niche for decades. A stock trading below book value, followed by barely four analysts, while simultaneously feeding the narrative of the quiet beneficiary of the humanoid boom. Klingelnberg sounds like the classic contrarian dream: a “picks-and-shovels” hidden champion, cheap, overlooked, with built-in upside fantasy. The nice part is that there is genuinely something fundamental to this picture.

Klingelnberg likely does benefit from the robotics boom. But it is an optionality that today is not yet as clearly visible as investors would like, and, this is the central sharpening of the thesis, it is a narrower and more concrete optionality than the bottleneck headline suggests. The company sits, with caveats we’ll name precisely, exactly where this bottleneck takes effect. In order: first the bottleneck itself.

The Bottleneck Bank of America Now Names Prominently

In its Institute report, Bank of America projects global humanoid robot deliveries to rise from roughly 18,000 units in 2025 to one million per year by 2030–2035. That corresponds to an annual growth rate of 88%. By the mid-2030s the bank expects ten million units per year, and in the steady-state view through 2060 even an installed base of three billion robots worldwide. You can halve or doubt these numbers. But even the conservative endpoint of one million units per year ten years from now would be a massive scaling versus today.

For this scenario to play out, the bank names three structural risks: first, regulation of embedded AI; second, availability of processor chips; and third, the point that interests us, availability of high-precision machine tools. Verbatim:

“Some precision parts of humanoid robots (such as planetary roller screws and harmonic reducers) require high-precision grinding tools for mass production, which are still dominated by a few European and Japanese companies. As such, the availability of high-end machine tools could potentially hinder the capacity expansion of humanoid robot components.”

Bank of America Global Research, April 2025

This is not a generic “capex risk.” The machines on which the precision parts of robot gearboxes are ground come globally from a handful of firms. Machines of this class cost around EUR 1–3 million each, with lead times of 12 to 24 months. The oligopoly cannot expand its output at will. If humanoid demand follows the volume path, this grinding layer will inevitably run hot and it is precisely this capacity mechanic that a Western supplier could benefit from.

One important clarification up front that runs through the rest of this text: the two component classes BofA names verbatim planetary roller screws and harmonic reducers Klingelnberg directly serves neither. Planetary roller screws are screw technology (Schaeffler/Ewellix, Schneeberger, Drake); harmonic reducers are made by Harmonic Drive Systems, which holds roughly 85% market share through vertical integration. Over 90% of today’s joint modules run on exactly these two architectures. The bottleneck for the grinding layer as a whole is real; how much of it specifically lands at Klingelnberg is a different question and the one this analysis is devoted to.

Who Even Plays This Listed in the West

These “few European and Japanese companies” can be counted on one hand. In the Western premium segment of precision gear-cutting machines, there are four names: Reishauer of Switzerland, Kapp Niles and Liebherr of Germany, and Gleason of the United States. All four are private. Reishauer and Kapp Niles are family- or foundation-owned, Liebherr is a family conglomerate, and Gleason was taken private from the NYSE in 2000.

With one single exception in the listed Western universe: a Swiss family business founded in 1863, listed on SIX, followed by barely four analysts, with a market capitalization of roughly CHF 100 million Klingelnberg AG. Anyone wanting to play the bottleneck Bank of America has named through the public markets has, in the West, exactly this one option. The only other globally listed direct competitor is the Chinese state-owned company Qinchuan the embodiment of the counter-thesis that China will close the gap. In Japan, Nidec Machine Tool (TYO: 6594, estimated ~60% domestic market share) adds itself to the list, but as an embedded division of a diversified conglomerate it is not a pure play.

What Klingelnberg Actually Sells

Klingelnberg is neither a robot builder nor a gearbox manufacturer. The company supplies the machines that others use to make their gears. It is a second-stage equipment supplier on the razor-and-blades principle: high-priced machines, plus tooling, the KIMoS software, and a profitable service and retrofit business all interlocked into a closed ecosystem with over 200 issued patents.

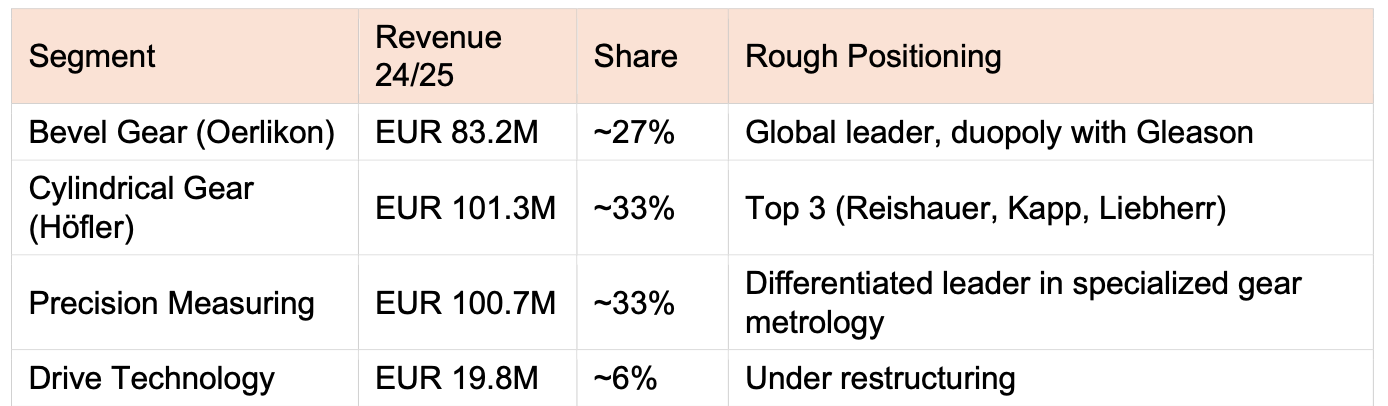

Four product lines carry the group. The centerpiece is Bevel Gear Technology, where Klingelnberg shares practically the entire Western premium market with Gleason. Alongside that sit Cylindrical Gear Technology (Höfler), the Precision Measuring Centers (metrology), and the small Drive Technology unit, currently being restructured. In the record year 2024/25 the group posted revenue of EUR 309 million, EBIT of EUR 16.2 million, and a margin of just 5.2%. About 51.9% of revenue came from the Asia-Pacific region and another 30.0% from EMEA.

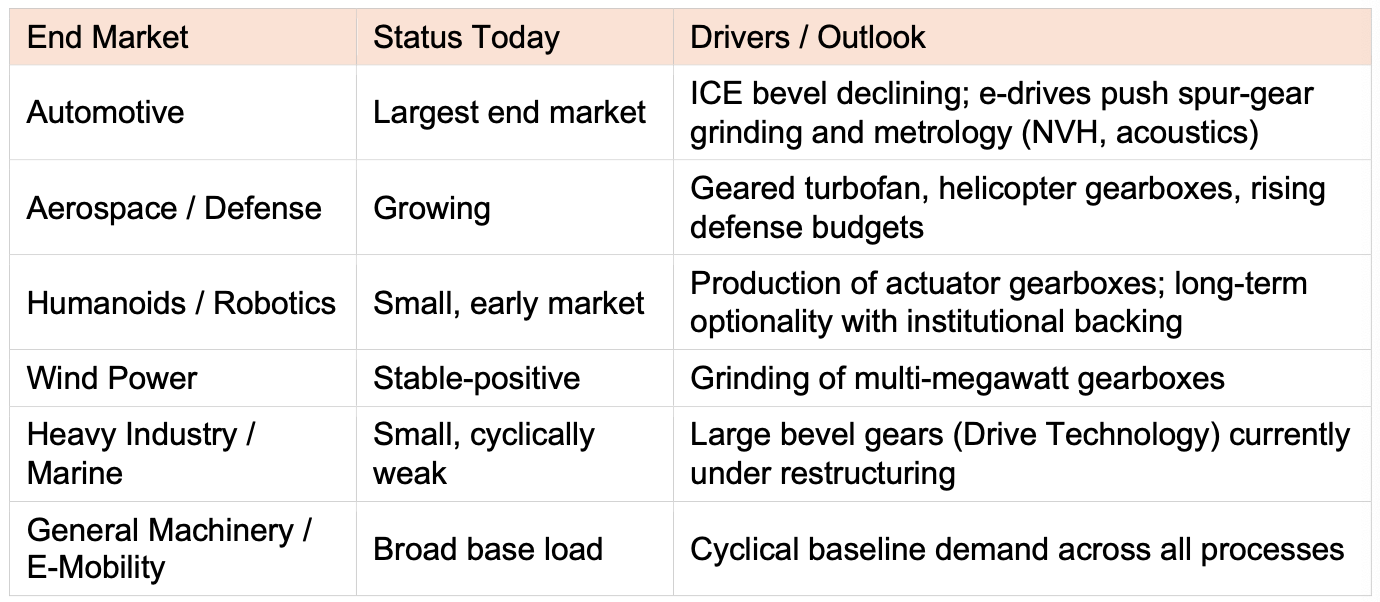

The End Markets at a Glance

Klingelnberg does not sell its machines into a single market. Demand is spread across several end industries, and this diversification is the lever that can make the company less dependent on the pure automotive cycle over time.

The Growth Trends in Detail

Two trends carry the growth narrative beyond the classic automotive business. Both are real, but they carry different distances.

Aerospace and Defense: Currently the Most Credible Growth Trend

Management itself names aerospace and defense as the most important growth market. Specifically, this means helicopter gearboxes (both civilian and military), which are bevel-gear intensive here Klingelnberg’s core strength pays off. On top of that come engine auxiliary gearboxes, GTF reduction stages, landing-gear and tiltrotor mechanisms, plus 100% quality inspection of safety-critical parts. The base is small (estimated 5% to 15% of revenue) and adoption is slow, but anchored in the machine portfolio and the backlog. With the G 35, a two-spindle bevel-gear grinding machine for the fixed-setting 5-cut process, Klingelnberg has an aerospace-specific dedicated machine in its lineup; the process lock-in through certification additionally raises switching costs. Once you have a helicopter or GTF manufacturer as a customer, you keep them for decades.

Humanoids: The Logic, and Where It Narrows

The logic sounds compelling at first. A humanoid robot has, depending on the design, 28 to over 40 joints, and almost every one of them contains a precision gearbox. For the arm to grip precisely and without jerk, the gears must be manufactured to extreme accuracy to a few thousandths of a millimeter, in hardened steel. This precision level is achieved only through grinding, and that is exactly Klingelnberg’s domain. Klingelnberg addresses this with real products: the VIPER 500 for grinding cycloidal discs (Klingelnberg heartland), the Speed Viper for the small spur gears in the reduction stages (challenger zone against Reishauer), and the P-series measuring machines for quality assurance (also heartland).

So far, the positive picture. A manufacturer-by-manufacturer review of the humanoid field around 30 programs nevertheless forces a sharpening that makes the case both more honest and more concrete. It can be summarized in three findings.

First: architecture is the first filter, and it eliminates most of the field. Industry consensus is that more than 90% of joint modules use harmonic (strain-wave) or planetary gears harmonic dominates the upper body and compact joints, planetary the more heavily loaded lower extremities. Harmonic is not a Klingelnberg process (Harmonic Drive Systems is vertically integrated). Planetary roller screws for linear actuators (Tesla, XPeng, Kepler, Apptronik) are screw technology, fully outside the gear-cutting business. What remains for Klingelnberg are only the planetary stages (grindable on the Speed Viper) and the cycloidal/RV discs (grindable on the VIPER 500, with cycloid metrology on the P-series).

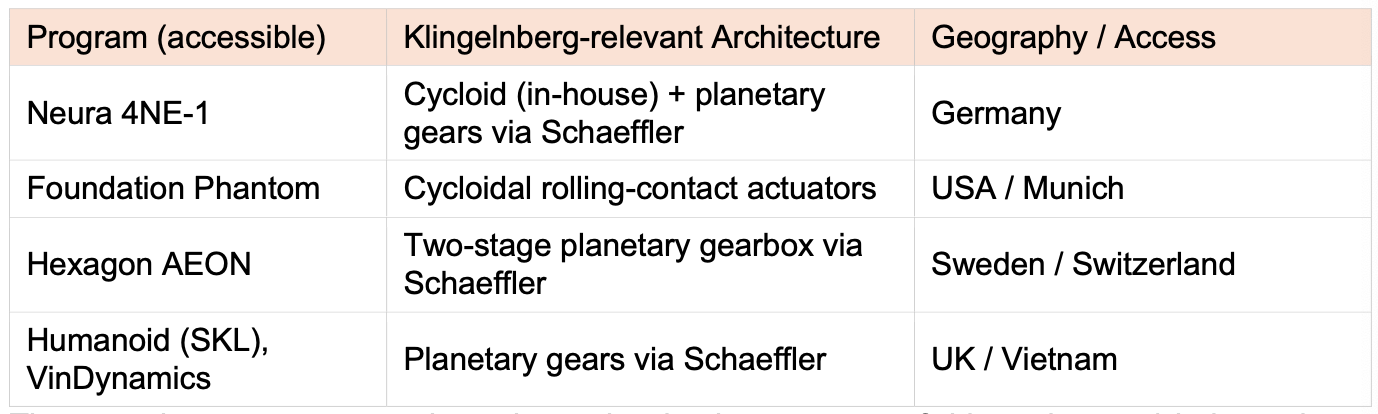

Second and this is the trend that most strongly favors Klingelnberg: cycloid is coming, but it is at the very beginning. Several Western premium programs are moving toward cycloidal gearing, because it combines harmonic-like precision with planetary-like robustness. This is no longer abstract capability there are concrete, verifiable names: Neura Robotics (4NE-1) uses, per its CEO, cycloidal gear drives that double torque in the same packaging from around 150 to over 300 Nm per joint (leg joints up to ~490 Nm). Foundation (Phantom) uses cycloidal “rolling-contact” actuators with claimed 90–95% efficiency versus 50–60% for harmonic. This exact architecture lands on the VIPER 500. The caveat: cycloid is only just being validated in humanoid joints; it is a real but partial shift, concentrated on Western premium designs.

Third: geography is the second filter, and it concentrates the accessible opportunity in Europe. The unit volumes lie in China Unitree and AgiBot alone are likely to account for roughly 80% of Chinese deliveries in 2026 but Chinese manufacturers localize their supply chains and buy domestic grinding machines (Qinchuan and competitors). Even where their architecture is Klingelnberg-relevant (planetary quasi-direct drive), the supply chain is effectively closed to a Swiss premium supplier.

Combining both filters relevant architecture AND Western-accessible supply chain leaves not the whole BofA volume, but a handful of programs. This subset is the honest, directly addressable base of the thesis:

The most honest sentence about the entire thesis came out of this review and belongs here: “grindable” is not “sold.” No public source confirms a Klingelnberg machine on a humanoid reducer production line. This analysis maps where the opportunity could realistically exist not confirmed sales.

The critical flip side remains the Tier-2 position: Klingelnberg sells the machine once, not the gearbox installed dozens of times per robot; a grinding machine produces hundreds of thousands of parts over its life. The value components belong to others Nabtesco (RV/cycloid, around 60% of industrial robot reducers) and Harmonic Drive (strain wave).

On top of this sits a transparency gap that needs to be named openly: whether robotics generates any revenue today is impossible to quantify from the outside. Klingelnberg reports by product segment (Bevel, Cylindrical, Measuring, Drive), not by end market a “Robotics” line does not exist in the financial reporting. Realistically, some industrial robotics revenue is already flowing, but invisibly booked into the segment figures; humanoid-specific revenue, by contrast, is practically zero and unconfirmed. The company’s own communication is telling: Klingelnberg’s appearance at the leading EMO Hannover trade fair (September 2025) put automotive eDrive and metrology in the foreground humanoids did not appear in the product highlights. Robotics is therefore optionality today, not a disclosed revenue driver.

The Missing Hinge of the Thesis: Schaeffler

Anyone wanting to play the bottleneck has to answer a question the bottleneck headline lacks: through which customer should humanoid demand reach Klingelnberg at all, if the two most prominent component classes (PRS, harmonic) run past Klingelnberg? The most plausible answer is Schaeffler and it deserves more room here than most analyses give it.

Schaeffler is Klingelnberg’s competitor in the PRS world (through Ewellix). On the planetary and cycloid side, however, the company is something different: it manufactures its actuators in-house. Its CES 2026 actuator combines a two-stage planetary gearbox with motor, encoder, and controller (torque range 60 to 250 Nm). Anyone manufacturing planetary and cycloidal gears in-house is a buyer of gear-grinding machines, not a buyer of gears and that is the textbook opportunity for Klingelnberg. Schaeffler quantifies its own addressable share at roughly 50% of a humanoid’s bill of materials and cites 25 to 30 actuators per robot on average.

The connection is not speculation: Schaeffler states it collaborates with around 45 humanoid players (five firm contracts, the largest in China and the U.S.) and has actuator supply agreements with Neura, Hexagon (AEON), Humanoid/SKL Robotics, and VinDynamics, plus a minority stake in Agility. With that, Schaeffler is the common denominator of nearly all Western-accessible Bucket-A programs above. Klingelnberg’s most realistic humanoid path runs not through the robot makers directly, but through the European Tier-1 actuator suppliers that cut their own gears Schaeffler above all.

From this follows the most valuable unanswered question of the entire case: which gear-grinding machines does Schaeffler (and Neura) buy for its in-house planetary/cycloid lines and from whom? No public source names the supplier. The entire upside of the humanoid thesis hangs on this single verification. It is therefore not just a footnote, but the most precise trigger this case knows (see watchlist).

The Competitive Position in Detail: Where Klingelnberg Really Stands

The robotics thesis does not stand or fall on whether Klingelnberg is a “machine builder,” but on whether, in the specific processes that robot gearbox makers need, it has a defensible position. That requires the most important geometric distinction, briefly.

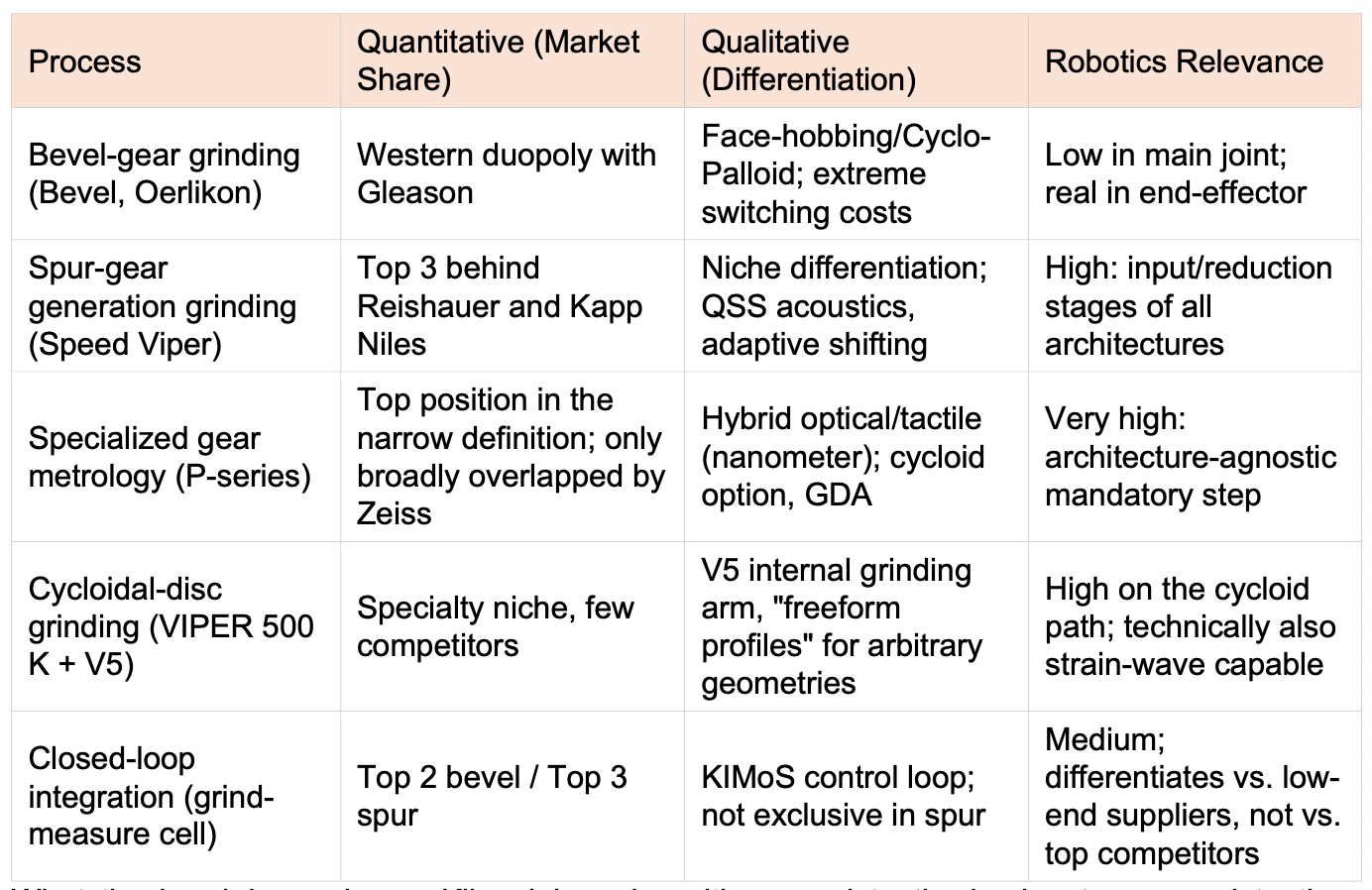

Bevel gear. Two gears positioned at an angle to each other, transmitting force “around the corner.” Klingelnberg’s quasi-monopoly area. Almost irrelevant for humanoids in the main joint (where coaxial specialty gearboxes run), but relevant in the end-effector for TCP positioning. Spur gear. The classic round gear, ground on the Speed Viper, robotics-relevant in the input and reduction stages of actuators but here Reishauer is world market leader and Klingelnberg the challenger.

What the breakdown shows: Klingelnberg is neither consistently dominant nor consistently a laggard. There is a heartland zone (bevel, gear metrology, cycloidal-disc grinding) where Klingelnberg leads qualitatively and in parts quantitatively, and a challenger zone (spur-gear generation grinding, closed-loop in spur) where Reishauer and Kapp hold the upper hand. The robotics exposure spans both zones and the two most robust threads, metrology and cycloid grinding, sit squarely in the heartland.

The Moat Is Real, but Defensive

In the bevel gear business, the protective wall is real and deep. A move away from the Klingelnberg system means a complete switch of tools, software, programmers, and training. These switching costs are enormous the actual quasi-monopoly core. On top sit an installed base built over six decades and iconic industry names such as “Oerlikon Bevel” and “Höfler.”

The nuanced read: part of the bevel business hypoid bevel gears for combustion-engine rear-axle differentials is structurally shrinking with the EV transition. Often overlooked: first, the e-axle absorbs a significant share again, because it imposes higher NVH requirements; precise spur-gear grinding (Speed Viper) and metrology (P-series) are mandatory there, both heartland. Second, performance AWD e-axles retain bevel components for disconnect systems and torque vectoring. Third, and quantitatively most important, the bevel moat simultaneously sits in structurally growing end markets: helicopter gearboxes (aerospace backlog around 11 years), industrial gearboxes, mining drives, marine propulsion, and now humanoid end-effectors. The moat is therefore defensive in the combustion-engine passenger-car path, but at the same time transferable to several growing end markets.

What cushions the EV pressure is the speed of repositioning. At its core, Klingelnberg is a build-to-order assembler of configurable platforms, not a series producer with fixed lines. The product mix can be shifted comparatively quickly from weak ICE automotive toward sought-after robotics, aerospace, and e-mobility machines, without rebuilding production lines. This structural flexibility is an undervalued advantage, precisely because it is hard to see from outside.

Notable is the lead time of the positioning: the white paper “Precision in Robotics through the Klingelnberg Production System” (2018) explicitly names robotics as a target market, with three addressed application fields and concrete machine recommendations bevel geometry in the end-effector (TCP positioning), the spur gears in the reduction stages (Speed Viper), and possibly most important, cycloidal gearing for eccentric gearboxes (i.e., directly the Nabtesco architecture) on the VIPER 500 K with the V5 internal grinding arm and “freeform profiles” software for non-involute profiles. That shifts the credibility of the intended positioning not the visibility of actual revenue. Klingelnberg is not coincidentally suited to robots; the company has been deliberately positioning itself for this for at least seven years.

The Central Mechanism: How the Bottleneck Works for Klingelnberg

Bank of America’s finding states that the machine bottleneck exists. It does not explain how it translates into order intake and pricing power for a single supplier. Precision matters here and specifically in two separate statements that short analyses tend to merge.

Statement 1 (applies without restriction): the grinding layer as a whole wins, regardless of actuator architecture. Whether planetary roller screws, cycloid, or strain-wave gears prevail somewhere a precision grinding step is needed on those EUR 1.3 million machines with 12 to 24 months of lead time. This bottleneck sits above the architecture fork. If robotics scales to the projected volumes, the entire grinding layer runs hot: lead times explode, prices rise by a factor of two to five, and the marginal customer buys wherever there is any capacity at all. This is a real mechanism, familiar from semiconductor and battery-equipment cycles.

Statement 2 (applies only with restrictions): how much of that specifically reaches Klingelnberg is capped. This is the central correction to the naïve read. Klingelnberg only captures one side of the bottleneck BofA names. The PRS side the dominant lower-body path and a major share of actuator costs belongs to screw-drive specialists (Drake, Schneeberger, EMAG, primarily Schaeffler/Ewellix); Klingelnberg does not play there. The harmonic side is vertically integrated at Harmonic Drive Systems. Klingelnberg captures the gear side planetary and cycloid stages via Speed Viper and VIPER 500 and in the robotics-relevant spur it is the challenger behind Reishauer. In the squeeze everyone benefits, but the process market leader disproportionately so. Klingelnberg’s share of the squeeze gain is therefore structurally capped: by the processes it plays in, and by its position within those processes.

From this follows the clean formulation of the thesis, which protects against the obvious bear case: this is a capacity and pricing bet, not a unit-share bet. The trade is not “Klingelnberg wins every humanoid robot,” but “with tight grinding capacity and rising gear demand, the market clears first on price, then on machine orders and some of that flows down even in the challenger zone.”

An additional, net mildly positive micro-point: some designs may switch the load-bearing leg joints from harmonic to planetary gears (higher shock resistance, lower price). This shifts machine demand away from the flexspline internal-gearing world, where Klingelnberg is weakest, toward the spur-gear world, where the Speed Viper plays not into the monopoly heartland, but into Klingelnberg’s stronger position.

The Decisive Asymmetry: The Chinese Overflow Valve

The capacity squeeze only works as long as there is no valve absorbing demand. Exactly that valve is being built in China and fastest in the cylindrical and EV segment, that is, where Klingelnberg’s Speed Viper sits. Machine tools are prioritized as a strategic bottleneck technology in Beijing’s five-year planning; Chinese gear-grinding machines for robot joint reducers already exist, at a fraction of Western prices. If prices in the squeeze rise by a factor of two to five, that is exactly the moment when a Chinese grinder starts to look “good enough.” The pillar still holds in the top precision segment, but the gap is closing fastest exactly where the robotics lever sits.

Worth noting: in the same report, BofA assumes “mostly Chinese-made components, if possible” as the base case for its unit-cost arithmetic and projects BOM costs falling from roughly USD 35,000 to USD 13,000–17,000 by 2030–2035. The source that validates the bottleneck thesis simultaneously assumes its biggest long-term threat. For Klingelnberg this means: the trade is not “robotics gets big, therefore Klingelnberg is perpetually strong,” but “robotics scales in a window during which the Western oligopoly still has pricing power, before China catches up.” Pointedly: the moat is protected from China but barely relevant for robotics; the robotics lever is relevant but most threatened by Chinese localization.

The Systems Argument: Can It Be Deepened?

One could argue that Klingelnberg is a superior systems supplier a self-correcting grinding/measuring cell with a closed control loop that no one else offers at this depth. Does that hold? Only partially. Closed loop is a duopoly or trio feature, not a Klingelnberg USP: in the spur-gear segment it is none other than market leader Reishauer who masters it, in series and through the open GDE format even interoperable with third-party metrology. The integrated system differentiates the top suppliers from the rest, not Klingelnberg from its direct competitors.

But: metrology is the single most convincing robotics thread, and here Klingelnberg leads. As the only component, it is architecture-agnostic it measures every gear type and is a mandatory step, regardless of who grinds and which design wins. It thereby captures robotics demand without architecture risk. In specialized gear metrology, Klingelnberg is a differentiated market leader (P-series as the industry-wide reference, hybrid metrology, cycloid option); Zeiss leads in universal coordinate metrology, not specialized gear metrology. For the robotics use case the narrow definition is the relevant one and this is probably the most underrated lever in the entire case. Caveat: even here Gleason and Wenzel are serious competitors, the revenue lever per machine is smaller than for grinding machines, and large customers increasingly build their own QA in-house.

The Structural Core Risk Remains the Powertrain Transition

Even without China, the EV transition is double-edged. Positive: electric drives are more noise-sensitive than combustion engines; this drives investment into spur-gear grinding and metrology Speed Viper and P-series benefit structurally. Ambivalent: within the heartland, the mix shifts from hypoid bevel toward cylindrical spur and toward the P-series. In the passenger-car path this means more competition against Reishauer, but also higher precision requirements per vehicle. Negative: the transition is taking place in a more contested cylindrical environment than the bevel duopoly. How sharply this hits margins depends on how quickly aerospace and robotics offset the mix shift. The weak margin in H1 25/26 shows that this dynamic is playing out right now before the growth end markets push back tangibly.

The Numbers: Cheap, but for a Reason

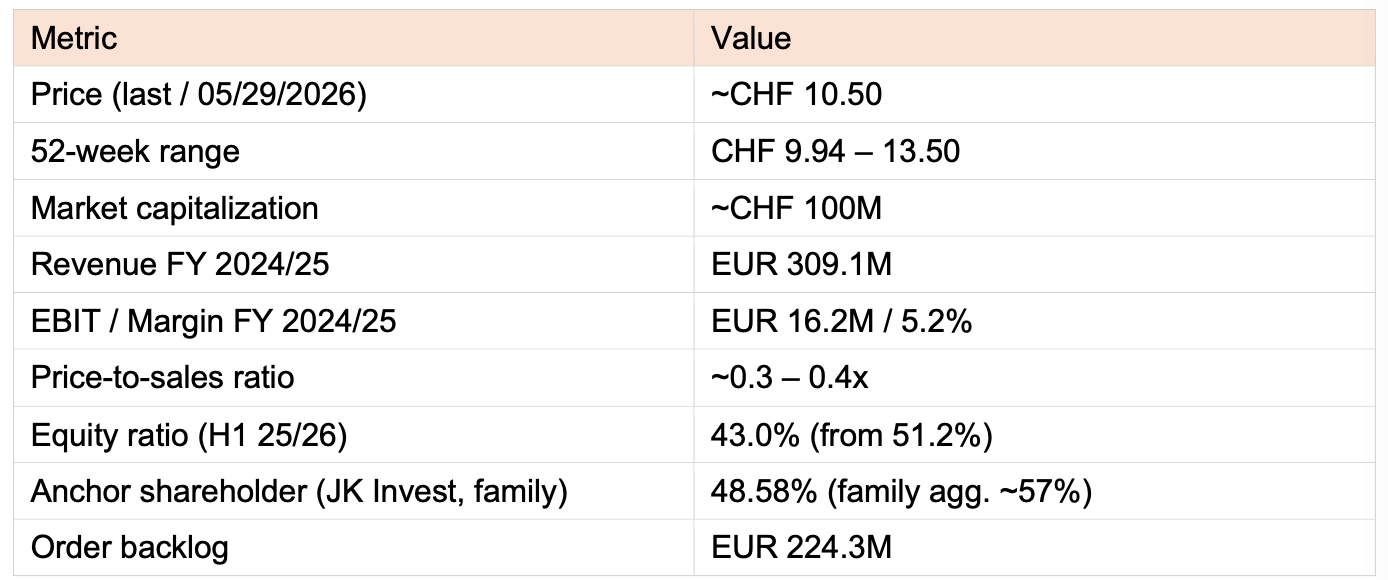

The current fiscal year has noticeably cooled. In H1 2025/26 revenue fell 18% to EUR 103.6 million, EBIT slid to EUR -13.3 million, and net loss came in at EUR -14.6 million. The balance sheet draws particular attention: equity ratio dropped within half a year from 51.2% to 43.0%. The good news sits alongside: order intake jumped 18% to EUR 119.6 million, with bevel order intake even up 45%, and the backlog stands at EUR 224.3 million. Management confirms a positive full-year result. Klingelnberg typically books only 30% to 40% of annual revenue in the first half so the losses are partly seasonal, but the absolute decline is disproportionate.

The stock currently trades between CHF 10.00 and CHF 11.00, with a market capitalization of about CHF 100 million. Optically cheap: a price-to-sales ratio around 0.35 and in places near book value. But careful: this P/S and the FCF yield are based on the peak year FY 2024/25, while the company is currently posting losses. “Below book” is less reassuring when book value is actively eroding. The only sensible view is a normalized mid-cycle one and on that basis Klingelnberg is reasonably valued, but no longer a bargain. The scarcity premium as the only listed Western pure-play is real, but it tempts you to underestimate the idiosyncratic risk: there is simply no comparable peer to cross-check against, and the listed “robotics plays” (Nabtesco, Harmonic Drive, Schaeffler/Ewellix) are not Klingelnberg’s competitors but its potential customers.

Trading below book value is less reassuring when book value is actively eroding.

The only meaningful approach is a normalized mid-cycle view, and on that basis Klingelnberg is reasonably valued, but no longer a bargain. The scarcity premium as the only listed Western pure-play is real, but it also encourages underestimating idiosyncratic risk: there is simply no comparable peer for a proper cross-check, and the listed “robotics plays” (Nabtesco, Harmonic Drive, Schaeffler/Ewellix) are not competitors of Klingelnberg, but rather its potential customers.

Risks

Equity is eroding: ratio has dropped from 51.2% to 43.0%; below 40% it gets serious.

Asia concentration risk of roughly 52% brings tariff and geopolitical exposure.

Highly concentrated shareholder base: JK Invest holds 48.58% directly, with related holders around 57%; free float and liquidity are thin, analyst coverage minimal.

Pronounced cyclicality: order intake has historically swung between EUR 90 million and EUR 311 million.

Site concentration: production at a few locations in one region; the 2021 flood in Hückeswagen showed what that can mean.

Robotics-specific: “grindable” is not “sold” no disclosed humanoid revenue; and the Chinese overflow valve sits squarely in Klingelnberg’s challenger zone.

To say it plainly: this is not a defensive compounding investment, but a cyclical special-situation stock with attractive optionality.

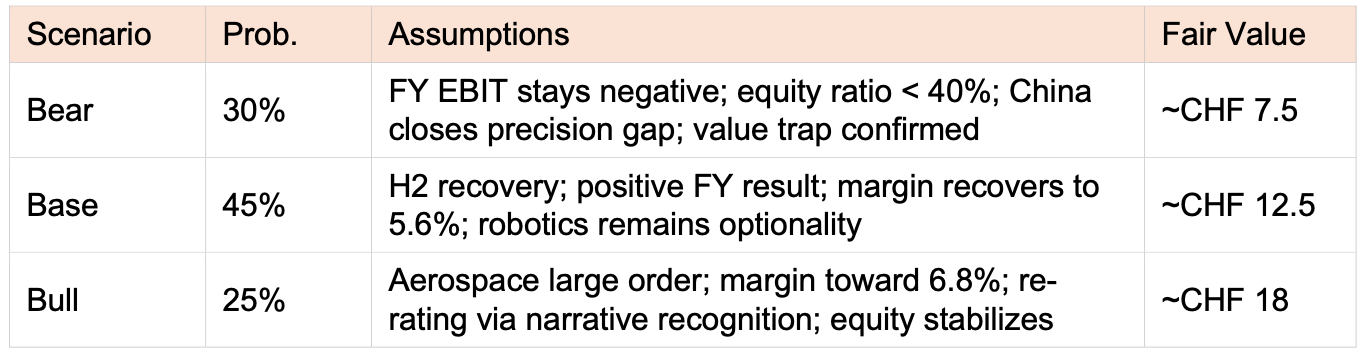

Scenarios

Three paths, honestly weighted. Fair value is not a point estimate but a range. The humanoid optionality deliberately plays no role here simply because we cannot seriously quantify it at this point; it is upside beyond the scenarios.

The Conclusion

Klingelnberg is a cyclical quality niche leader with a genuine but defensive moat, moderate aerospace optionality, and a robotics narrative that is institutionally backed by BofA but structurally capped by Chinese localization in exactly Klingelnberg’s relevant segment. This is not a pure AI-robotics play, but it should not be priced as a pure auto cyclical either.

The most important sharpening: The robotics optionality is narrower and more concrete than the bottleneck headline suggests. It does not rest on a “broad bottleneck across all architectures,” but on three precisely nameable pillars the architecture-agnostic metrology (P-series), cycloid grinding (VIPER 500) with concrete Western early indicators such as Neura and Foundation, and the Schaeffler question as the decisive, still-unverified hinge. Cleanly framed, the thesis is a capacity and pricing bet, not a unit-share bet. That does not make it weaker, just more honest and armored against the obvious bear case.

Can robotics plus the e-mobility shift plus aerospace replace the combustion bevel business? The combustion bevel path does not fall away without a replacement; it migrates into three parallel drivers: the e-axle spur gear (Speed Viper, running now), NVH metrology (P-series), and the genuine growth end markets aerospace and robotics. Even if the 10-million-unit path is conservatively halved, the humanoid mechanism alone adds a double-digit percentage to global gear-grinding-machine demand. The Tier-2 dampening scales that down but does not eliminate the effect.

My personal impression: Klingelnberg is a classic hidden champion in European mechanical engineering that is currently going through a cyclical downturn. The structural threat from the decline in the combustion business is real and so are the new demand drivers from aerospace and defense. And the humanoid / robotic optionality remains one of the most attractive I currently see in the European small-cap universe, provided you price it as what it is: a narrow, high-quality heartland lever plus a Schaeffler bet, not a broad bottleneck free pass.

Those who read me for longer know: I tend toward neither euphoria nor overstatement. At the current price, the market gives a margin of safety of roughly 15%. Anything beyond that, Klingelnberg first has to deliver. The Bank of America study opens the imagination space, the China risk remains real and must be taken seriously and the hardest proof of the robotics thesis is still pending: a disclosed grinding-machine sale into a real humanoid actuator line.

SIX: KLIN · ISIN CH0420462266

Disclosure: The author holds a position in Klingelnberg. No positions are held in other securities mentioned. The author has received no compensation from any company mentioned or third parties. No transactions were made in the 72 hours prior to publication, and no sale is planned within the 72 hours following publication. Any exceptions (material new information) will be disclosed promptly.

Disclaimer: This article is based on publicly available information and reflects the personal opinion of the author. It does not constitute investment advice, an investment recommendation, or a solicitation to buy or sell securities. The author is not a regulated or licensed person under MiFID II, FinfraG, or comparable frameworks. Investing in equities involves substantial risk, including total loss of capital. Forward-looking statements are uncertain; past performance does not predict future results. Readers must conduct their own research and consult a qualified adviser before making investment decisions. Liability for losses arising from the use of this information is excluded to the extent permitted by law.

One paragraph is repeated:

The stock is currently trading between CHF 10.00 and CHF 11.00, giving it a market capitalization of roughly CHF 100 million. On the surface, it looks cheap: a price-to-sales ratio of around 0.35 and at times trading close to book value. But caution is warranted: both the P/S multiple and the free cash flow yield are based on the FY 2024/25 peak year, while the company is currently reporting losses. Trading below book value is less reassuring when book value is actively eroding.

Another company worth considering is Okamoto Machine Tool Works from Japan. This company is a confirmed supplier of precision grinding machines to Harmonic Drive. Their strenght is highly scalable production systems by combining specialised grinding machines which enables the manufacturing of final parts with much reduced lead times.